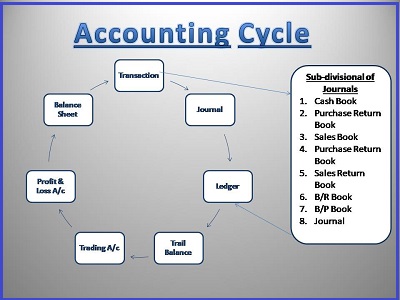

Accounting Cycle

Accounting Cycle is that cycle in which all the business transaction are recorded, classified and summarized. It is also known as Accounting Standards.

It is the process of recording all the transaction in following way:

- Books of original entry: firstly all the business transaction is recorded in the books of original entry, called as Journal. In this book all the transactions are recorded as per the 3 Golden rules (Real account, nominal account and personal account).

- Journal is sub divided into ‘sub-journal’ or ‘subsidiary books’.

- Classification or Ledger posting: All the transaction recorded in the Journal or in the subsidiary books are transferred (posted) to various Ledger accounts. In this process, date wise recorded transactions are classified item wise. Thus, this is the second stage of recording and all the separate accounts are made as per item given.

- Summary: At the end of the accounting period all the ledger account are balanced and these shows the balances are zero on both side of debit side and credit side.

- A list prepared in the form of debit balance and credit balances, called as Trail Balance.

- If all the recordings and postings and balances are correct then financial statements or final accounts are prepared.

- Final accounts are prepared to know the financial position of the Business Organization. In final accounts we prepare 3 accounts:

- Trading Account

- Profit and Loss Account

- Balance Sheet